Did you know that 83% of Americans overspend? This staggering statistic highlights the importance of having a well-planned monthly budget. By prioritizing your monthly expenses, you can avoid wasting money on unnecessary items and achieve financial stability.

Whether you’re rocking a six-figure salary or carefully budgeting each paycheck, understanding your monthly expenses is your golden ticket to financial freedom. It’s about making your money work for you – not the other way around.

Decoding Your Monthly Expenses: A Deep Dive

For many, the phrase “monthly expenses” conjures up images of daunting spreadsheets and confusing financial jargon. But I’m here to break it down simply.

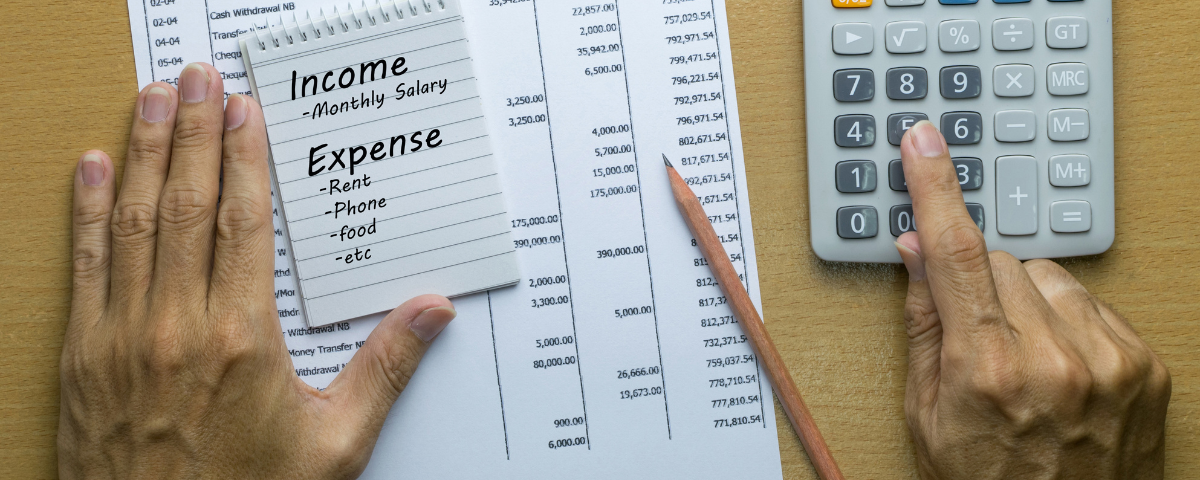

What Are Monthly Expenses (and Why Should You Care)?

Monthly expenses are simply the money you shell out each month to keep your life running smoothly. This isn’t just your rent or mortgage; think groceries, those streaming services you enjoy, car payments, that daily latte; it all adds up.

Understanding these expenditures is key to building a stable financial future. It’s like assembling a puzzle; by seeing the bigger picture, you can identify areas to save, reach your financial goals faster, and even sleep a little better at night.

The Usual Suspects: Breaking Down Common Living Expenses

While everyone’s financial situation is as unique as a fingerprint, some recurring culprits always pop up on the average monthly expense list. Let’s shine a light on the usual suspects:

- Housing: Often the biggest chunk of change goes towards keeping a roof overhead, whether it’s rent or a mortgage.

- Transportation: From car payments and insurance to bus fare or gas, getting around comes with a price tag.

- Food: This includes groceries, takeout, that morning coffee, or those delightful dinners out.

- Utilities: Lights, water, heat; basic necessities that make up a significant portion of anyone’s expenses.

- Debt Payments: Think credit card debt, student loans, auto loans, personal loans. These can eat a sizable portion of your income.

- Healthcare: Health and life insurance, doctor’s visits, and even that over-the-counter medication; staying healthy isn’t always cheap.

- Entertainment: Movies, concerts, streaming subscriptions, or hobbies. We all deserve some fun, right?

- Personal Spending: The “miscellaneous” category covers anything from clothing and beauty supplies to gifts and gym memberships.

Outsmarting Your Monthly Expenses: Proven Strategies

Now that you understand common monthly expenses, let’s explore practical strategies to take control:

1. Create a Rockstar Budget (Without the Headaches)

A budget is the heart and soul of financial health; and no, it doesn’t have to involve complicated spreadsheets or endless calculations. Start by tracking your income and expenses for a month (even if you have to use those trusty sticky notes.). A budget calculator can help you add this up easily.

Then, prioritize essential spending (like rent) while setting aside a reasonable amount for “fun money” or unexpected costs. You’ll discover hidden spending patterns you never knew existed. This process reveals your unique spending habits so you can start strategically managing your money.

Determining Needs vs. Wants

Everybody has monthly expenses, right? It’s how you manage them that makes a difference in your budget. Think of it like this: Needs are things you have no choice but to spend money on, like rent, groceries and debt payoff. You can’t live without them. Wants are things that make life better, but you can live without them, like streaming services or that daily fancy coffee.

Creating a budget means you’re getting a handle on your cash flow, which is a good thing! But sometimes, it’s hard to tell the difference between a need and a want. Do you really need that expensive brand of jeans or would something else work just as well? That’s where your budget comes in.

Start by listing out all your monthly expenses. Then, put them into two categories: needs and wants. Be honest with yourself. This will give you a good picture of where your money is going.

2. Automate Your Savings

It’s all about outsmarting those pesky monthly expenses. Set up automatic transfers from your checking to emergency fund or savings account each payday. Think about it like a non-negotiable bill to your future self.

Starting small is perfectly alright. Consistency makes a big difference in building a safety net for unexpected costs. This ensures you’re constantly contributing to your financial goals, even amidst busy schedules.

Another way to automate savings is to use apps that round up your purchases to the nearest dollar and automatically transfer the difference to your savings account. Let’s say you buy a coffee for $3.75. The app would round the purchase up to $4.00 and tuck away that extra $0.25. It might not seem like much at first, but those small amounts add up over time.

3. Negotiate Like a Pro

Believe it or not, monthly expenses aren’t always set in stone. Don’t be afraid to channel your inner negotiator.

Call your internet provider or insurance company; often, a simple phone call can uncover hidden discounts, promotions, or more favorable rates. It’s worth the effort. Remember, loyalty to companies often only goes one way; don’t hesitate to explore competitive options.

Tips for Negotiating Bills

First, do your research. See what other companies offer. Then, call customer service. Be polite but firm. Explain that you’re looking for a better rate. The worst thing they can say is no, right?

Don’t be afraid to ask for a supervisor if the first person you talk to isn’t helpful. Sometimes, supervisors have more leeway to make deals. If you’re persistent, you might be surprised at how much money you can save on your monthly expenses. This will help you manage your budget more effectively.

4. Trim the Excess Baggage

Remember that “miscellaneous” category in monthly expenses? Take a close look at your spending habits with a discerning eye. Are there any subscriptions you barely use? Impulsive purchases that you later regret?

Those “treat yo’self” moments can quickly add up, chipping away at your financial stability. Identifying and reducing unnecessary spending creates a financial cushion to reach your financial goals. Think of it as hitting the “reset” button on your finances, giving yourself room to breathe and achieve those money goals.

FAQs Related to Monthly Expenses

What is a typical monthly expense?

A typical monthly expense varies widely depending on individual lifestyle, location, and financial obligations. Generally, it includes costs for housing (rent or mortgage), utilities, food, transportation (car payments and fuel or public transit fees), insurance premiums (car insurance, life insurance, health insurance, etc.), healthcare expenses, debt repayments (such as student loans and credit cards), savings contributions, and discretionary spending such as entertainment. The exact composition and scale of these expenses are influenced by personal income levels, family size, geographical area of residence among other factors.

What are the 3 biggest monthly expenses?

The three largest monthly expenses for most individuals typically include housing, transportation, and food. Housing costs—such as rent or mortgage payments—generally consume the largest portion of a budget. Transportation expenses, which cover car payments, fuel, insurance, and maintenance, usually rank second. Food expenditures for groceries and dining out also represent a significant financial commitment each month.

What is the 50/30/20 rule?

The 50/30/20 rule is a simple budgeting guideline that helps individuals manage their finances effectively. According to this rule, you should allocate your after-tax income as follows: 50% towards necessities such as housing and groceries, 30% towards discretionary spending like entertainment and dining out, and the remaining 20% towards savings or paying off debt. This method provides a balanced approach to financial planning by dividing expenses into clear categories of needs, wants, and savings.

What is a good monthly spending?

A good monthly spending amount varies by individual circumstances but generally should align with the 50/30/20 budget rule. This guideline suggests allocating 50% of your net income to necessities, 30% to wants, and saving or investing the remaining 20%. It’s crucial to adjust these percentages based on personal financial goals, cost of living in your area, and income stability.

Conclusion

Taking control of your monthly expenses isn’t about deprivation; it’s about making conscious choices that align with your overall financial vision. Remember, every dollar spent represents a choice made. It’s not about penny-pinching; it’s about building the financial life you’ve always envisioned.